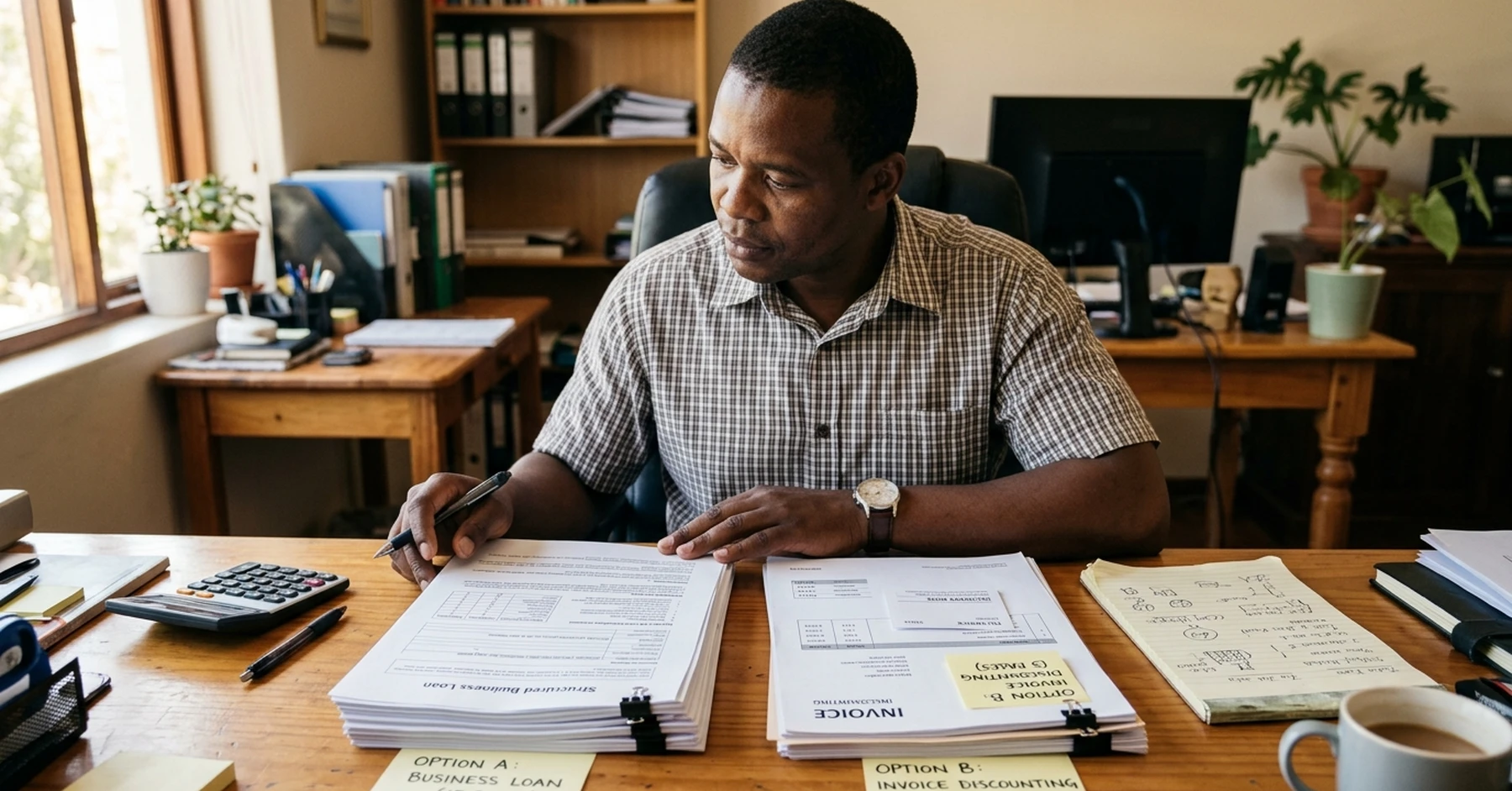

Invoice discounting vs short-term business loan is one of the most common funding questions SA SMMEs ask, and the honest answer is that the two products are built for different jobs. A short-term business loan gives the SMME a lump sum repaid over a fixed term from general business income, regardless of which customer pays which invoice. Invoice discounting is deal-based: the SMME advances cash against a specific customer invoice, and that customer’s payment of the invoice repays the funding. Different structure, different repayment source, different fit. The right tool depends on what the SMME actually needs the cash for.

Key Takeaways

- Invoice discounting vs short-term business loan is a structure-of-deal question, not a price question.

- A short-term business loan is a fixed-term commitment repaid from general business income.

- Invoice discounting is deal-based: it funds a specific customer invoice and is repaid when that customer pays.

- Invoice discounting suits SMMEs sitting on uncontested receivables from SA-based customers. Short-term loans suit SMMEs needing general working capital not tied to a specific receivable.

- Most Sourcefin invoice discounting deals start at around R250,000 because the structure works best at meaningful deal sizes.

The core structural difference: invoice discounting vs short-term business loan

The starting point in any invoice discounting vs short-term business loan comparison is the structure of the deal itself. The two products look similar on the surface – both deliver cash to the business – but they sit on completely different mechanics.

A short-term business loan is:

- A fixed-amount advance to the business

- Repaid over a fixed term (typically 3, 6, 12, or 24 months)

- Repaid in scheduled instalments from the business’s general cash flow

- Carried as a debt obligation on the business’s balance sheet for the life of the term

- Typically assessed on the business’s overall financial profile – turnover, cash flow, credit history

Invoice discounting is:

- An advance against a specific customer invoice

- Repaid when that customer pays the invoice – there is no fixed repayment schedule

- Self-liquidating on the deal it funds

- Assessed primarily on the invoice and the customer paying it, not on a long-term balance-sheet review

- Recorded against the specific receivable, not as a long-term debt obligation

What invoice discounting vs short-term business loan means for cash flow

For day-to-day cash flow, the structural difference matters more than the cost difference. A short-term loan adds a fixed instalment line into the cash-flow forecast – the business must make that payment every month regardless of which customers have paid that month. Invoice discounting moves with the deal: the cash comes in early against a specific invoice, and the customer’s payment of that invoice covers the funding.

Practical implications:

- Short-term loan: good for funding needs that are not directly tied to a receivable – buying equipment, covering a seasonal lull in trading, smoothing payroll across a quiet patch.

- Invoice discounting: good for funding needs that are directly tied to receivables – a long customer payment term has stretched the cash cycle, a single large invoice has tied up working capital, the business has won a contract and needs to fund the gap between delivery and payment.

For a related comparison, see invoice discounting vs bank overdraft in South Africa.

Assessment and documentation: what each product asks for

The application document set tells you a lot about how each product is assessed.

A short-term business loan typically asks for:

- Multiple months or years of business bank statements

- Annual financial statements and management accounts

- Personal financial information on the directors

- Business plan or turnover forecast

- Sometimes collateral or personal surety

Invoice discounting at Sourcefin asks for a focused, deal-based pack:

- CIPC documents and director ID

- The invoice(s) being discounted

- Proof of delivery or service completion

- Recent business bank statements

- Proof of business address and bank account

The full list is in invoice discounting documents required in South Africa. The difference reflects the difference in assessment: a short-term loan looks at the business as a whole; invoice discounting looks at the deal.

Cost: how the two products are priced

Both products carry a cost. A short-term business loan typically charges interest over the term plus an origination or set-up fee. Invoice discounting at Sourcefin charges a discount cost on the advance – no separate service fee. Comparing cost meaningfully requires comparing the total cost over the actual usage period, not headline rates in the abstract. Pricing depends on the deal, the customer, and the duration of the advance, so the only honest comparison is the actual quote.

What is worth flagging: invoice discounting cost moves with how long the customer takes to pay. If a 60-day invoice settles in 35 days, the funding cost is shorter. A short-term loan cost is fixed by the term, regardless of how quickly the business could have repaid early.

Invoice discounting vs short-term business loan: when to choose invoice discounting

Invoice discounting fits when:

- The cash-flow gap is tied to a specific customer invoice or a known receivables book

- The customer is SA-based and credit-credible

- The invoice is uncontested and the goods or services have been delivered

- The deal size is meaningful – most Sourcefin deals start at around R250,000

- The business has the operational capacity to retain the customer relationship and collections

Detailed eligibility lives in invoice discounting requirements in South Africa.

Invoice discounting vs short-term business loan: when to choose a loan

A short-term business loan fits when:

- The cash need is not tied to a specific receivable – equipment, premises, seasonal trading, growth investment

- The business has the steady income to service fixed monthly instalments

- The lender’s assessment of the overall business profile lands favourably

- The business is happy to take on a fixed-term debt obligation

Banks are the natural home for many short-term business loans, particularly for established businesses with longer trading histories. Banks are built for stability; specialist funders like Sourcefin are built for speed on specific deal-based finance. Both have a place. The question is what the SMME actually needs.

Where Sourcefin lands

Sourcefin has deployed R3 billion-plus in working capital to South African SMMEs since 2020, funded 1,000+ SMMEs, and maintained a 100% delivery rate on funded deals. The Sourcefin invoice discounting model is deal-based by design – which is exactly what makes it different from a short-term business loan.

For broader context, the Department of Small Business Development publishes SA small-business policy, and the IFC SME Finance Forum publishes the global MSME Finance Gap database covering emerging markets.

If your SMME is sitting on a customer invoice and the cash need is tied to that invoice, invoice discounting is probably the right tool. If the cash need is general and not tied to a specific receivable, a short-term business loan may fit better. Start at the funding application page or read more about how invoice discounting works at Sourcefin.

Sources & References

- SARS – South African Revenue Service, business compliance and tax guidance.

- Department of Small Business Development – SA small-business policy and reporting.

- IFC SME Finance Forum – Global MSME Finance Gap database, World Bank Group.

Frequently Asked Questions

What is the main difference between invoice discounting vs short-term business loan?

Structure and repayment. A short-term business loan is a fixed-amount advance repaid in scheduled instalments over a fixed term from general business income. Invoice discounting is deal-based – it advances cash against a specific customer invoice, and that customer’s payment of the invoice repays the funding. Different mechanics, different fit for different cash-flow needs.

Which is cheaper – invoice discounting or a short-term business loan?

Cost depends on the deal, not the product label. Invoice discounting carries a discount cost on the advance and no separate service fee on Sourcefin’s model. A short-term loan typically carries interest plus a set-up fee. The only meaningful comparison is the actual quote on the actual deal over the actual usage period, not headline rates in the abstract.

Does invoice discounting affect my SMME’s debt profile?

Invoice discounting is recorded against the specific receivable being funded, not as a long-term debt obligation on the balance sheet. A short-term business loan adds a fixed debt obligation for the life of the term. SMMEs that want to fund working capital without adding term debt often choose invoice discounting for that reason.

Can I use both invoice discounting and a short-term business loan together?

Yes, and many growing SMMEs do. The short-term loan covers cash needs not tied to a specific receivable – equipment, payroll, seasonal trading. Invoice discounting covers cash needs tied to specific customer invoices. The two products solve different problems on the same business, so they can run side by side.

How much can I get under invoice discounting vs a short-term business loan?

A short-term business loan is sized on the lender’s view of the overall business. Invoice discounting is sized on the invoice and the customer paying it. Most Sourcefin invoice discounting deals start at around R250,000, scaling with the value of the invoices being discounted and the credibility of the customer paying them.

What documents do invoice discounting vs short-term business loan applications need?

A short-term business loan typically asks for multiple months of bank statements, annual financials, management accounts, personal financial information, and a business plan. Invoice discounting at Sourcefin asks for a focused deal-based pack: CIPC documents, the invoices, proof of delivery, recent bank statements, and director ID. Different assessments, different document sets.