Purchase Order Funding Requirements South Africa: Real Guide

Wondering what you need to qualify for PO funding in SA? Here's the document checklist, the deal criteria, and the profile funders actually assess.

On this page

- Key Takeaways

- Purchase Order Funding Requirements South Africa: The Full Picture

- The Deal Requirements

- The Essentials

- To Move Faster (Send These Upfront)

- For Deals Over R1 Million

- The Three-Pillar Assessment Behind the Requirements

- SMME Profile: What Funders Look For

- What Disqualifies a Deal

- How the Requirements Compare to a Bank Loan

- The Bottom Line on PO Funding Requirements

- Frequently asked questions

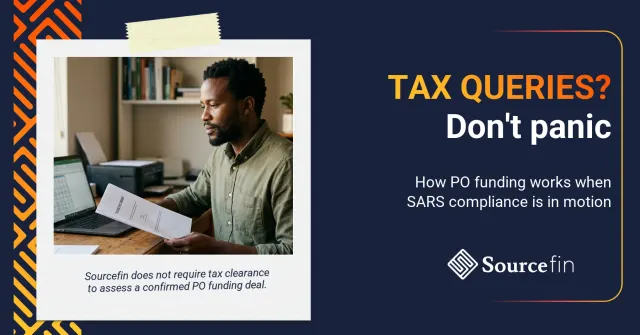

Purchase order funding requirements South Africa centre on three things: a confirmed deal, a clean compliance pack, and a credible delivery plan. You need a real PO or tender award, current SARS and CIPC status, recent business bank statements, and a supplier quote. Sourcefin assesses trust, delivery capability, and end-buyer payment certainty before approving an advance.

Key Takeaways

- The non-negotiable starting point is a confirmed purchase order or tender award letter from a credible buyer.

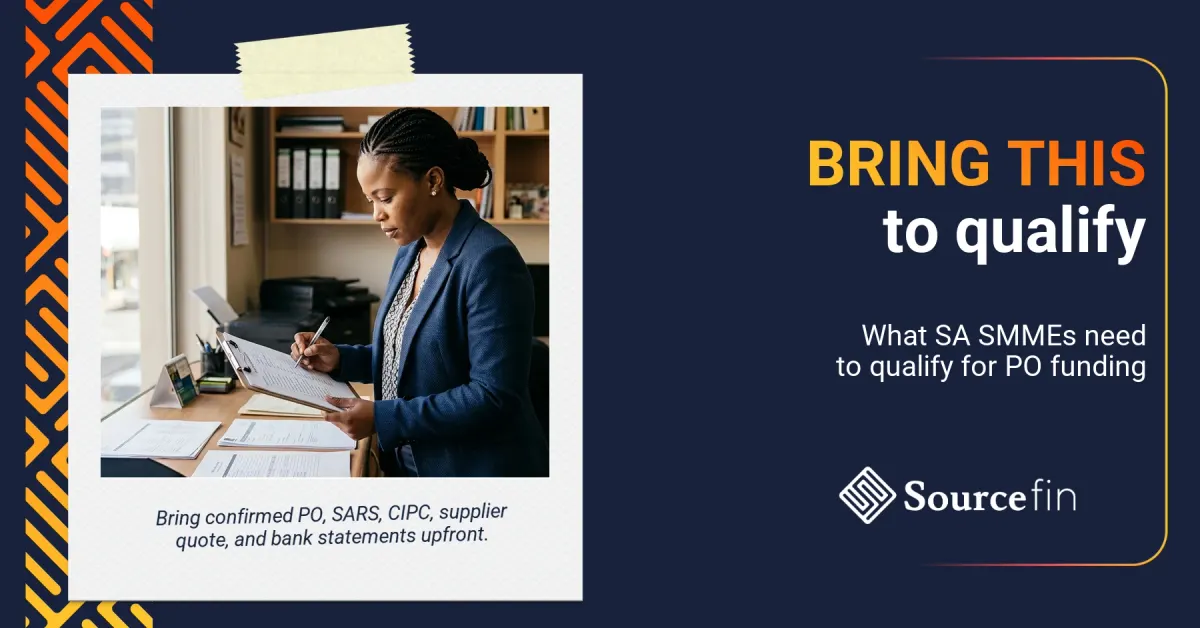

- Compliance pack: CIPC company registration in good standing, valid SARS tax compliance status, South African ID for directors.

- Financial pack: recent business bank statements (3 to 6 months), supplier quote or proforma invoice.

- Sourcefin's deal-size sweet spot is R250,000 upwards – smaller deals are usually a poor fit for the model.

- Personal credit is reviewed but does not auto-disqualify – the deal itself does most of the talking.

- The end buyer's payment ability matters as much as your own profile, often more.

Purchase Order Funding Requirements South Africa: The Full Picture

Purchase order funding requirements South Africa funders look at fall into three buckets: the deal, the compliance pack, and the SMME profile. All three need to check out for an advance to be structured. None of them is a deal-breaker on its own – but the absence of any of them stalls the application.

The deal sits at the centre. Without a real, confirmed contract, there is nothing to fund. The compliance pack is the operational hygiene that lets the funder transact with you. The SMME profile is the trust layer – who you are, how you have operated, and whether you are someone the funder can work with through the deal cycle.

For broader context on how the model works end to end, the wider purchase order funding South Africa pillar guide explains the approach. This article focuses specifically on what you need to bring to the table.

The Deal Requirements

Three deal characteristics determine whether a contract qualifies.

First, the contract must be confirmed. A signed purchase order, a written tender award letter, or an equivalent document from a credible buyer. Verbal commitments, draft documents, or expected awards are not enough. Funders need to see the deal on paper before they can structure an advance.

Second, the deal needs to fit the funder's size range. Sourcefin's typical deal range starts at R250,000 and runs through to multi-million-rand contracts. Smaller contracts are usually better served by an overdraft facility or short-term working capital from a commercial bank. The wider SMME funding alternatives overview covers options for sub-R250,000 deals.

Third, the deal needs to make commercial sense. There has to be enough margin between the contract value and the cost of delivery to absorb the cost of funding and leave you with a meaningful profit. Most PO funders look for at least a 20% gross margin on the underlying transaction. Razor-thin margins do not work for either side.

The Essentials

Sourcefin's document set is built in tiers. The first tier is the bare minimum needed to start.

- The purchase order, invoice, or award letter. The foundation of the deal. A signed PO or the official letter from the awarding department or corporate.

- CIPC company registration certificate. Confirms your legal entity exists and is in good standing. The CIPC website walks through how to retrieve or refresh registration documents.

These two are the foundation of the deal review. The application form itself only needs basic contact details and your funding amount – Sourcefin's representative will follow up by phone or WhatsApp to walk through which documents to send through. The PO and CIPC certificate are usually first.

To Move Faster (Send These Upfront)

The following documents are not strictly essential, but sending them with the initial application materially speeds the deal review.

- Tax PIN. A current SARS tax compliance status PIN. The SARS Tax Compliance Status guide explains how to retrieve or refresh it.

- Latest 3 months of business bank statements. Shows trading activity, cash flow patterns, and how you manage business funds.

- ID copies for directors and reps. Standard FICA requirement. Greenbar ID or smart card.

- Supplier quote or proforma invoice. The supplier's pricing for the goods or services you need to deliver against the PO. If you do not have a supplier yet, sourcing support may be available.

If your contract is a government tender, additional procurement-specific documents may apply – CSD registration, B-BBEE certificate or affidavit, and the relevant SBD forms. The purchase order funding for government tenders guide covers tender-specific requirements in more depth.

For Deals Over R1 Million

Larger deals need a slightly heavier financial pack to support the deal review.

- Management accounts for the past 3 months. Recent operational performance.

- Annual Financial Statements (no older than 18 months). Reviewed or audited, depending on the size of the business.

- Tax return summaries for the past 2 financial years. Shows the longer-term tax compliance picture.

The financial pack is where rigour pays off on bigger deals. Bank statements that show consistent trading activity – even modest – are a stronger signal than a polished pitch deck without supporting account history.

The Three-Pillar Assessment Behind the Requirements

The documentation requirements exist because Sourcefin assesses every deal against three pillars: trust, delivery capability, and end-buyer payment certainty. The documents feed into that assessment.

The trust pillar covers the SMME owner. Bank statement patterns, credit bureau history, prior business activity, and the conversation you have with the assessor all contribute. A credit issue does not auto-disqualify you – but how you talk about it matters. Disclosure with context consistently outperforms silence followed by discovery.

The delivery capability pillar covers the supplier and the operational plan. Can the goods or services actually be sourced, produced, and delivered on time and within budget? The supplier quote, your delivery plan, and any prior project experience feed in here. For complex deals, Sourcefin's in-house supply chain function (over 2,000 pre-vetted suppliers, plus a China sourcing office) can support this side of the deal directly.

The end-buyer pillar covers the contract and the buyer. Is the buyer financially sound? Do they have a history of paying suppliers? Is the contract real and enforceable? Sourcefin's portfolio is roughly 80% public sector, so the team has deep familiarity with how government departments, SOEs like Rand Water and Eskom, and major corporates operate.

SMME Profile: What Funders Look For

The SMME profile is the human layer of purchase order funding requirements South Africa. It is not a checklist in the same way the documents are, but it shapes the assessment significantly.

Funders look for owners who understand their own deals. If you can explain what is being supplied, who the buyer is, what the delivery timeline looks like, and where the risks sit, that signals operational competence. Vague descriptions or over-reliance on the funder to figure it out are warning signs.

They also look for owners who have done the upstream work. Lined up the supplier. Understood the buyer's payment terms. Read the contract. The applicants who arrive prepared move much faster through the process than those who arrive expecting the funder to fill in the gaps.

Past credit issues, prior business failures, or active legal disputes do not automatically rule you out. Context matters. Someone who had a judgment five years ago and has rebuilt their business looks very different from someone with active, unresolved disputes. The PO funding bad credit South Africa guide goes deeper on this scenario.

What Disqualifies a Deal

Some patterns reliably stop deals.

Speculative contracts – deals that exist only as expected awards or verbal commitments – cannot be funded. A funder needs paper. Deals where the buyer is unverifiable or has a history of payment disputes are rarely structured. Deals where the supplier cannot demonstrate ability to deliver are stalled until that piece is resolved.

On the SMME side, active legal proceedings related to fraud, asset stripping, or director misconduct are the strongest disqualifiers. So is dishonesty during the application – a credit issue you tried to hide is a much bigger problem than the issue itself.

How the Requirements Compare to a Bank Loan

Bank loans and PO funding ask for overlapping but different document sets. Bank loans typically require audited or reviewed annual financial statements, comprehensive director balance sheets, and security registrations on top of the standard compliance pack. PO funding leans heavier on the deal-specific documents – the actual purchase order, supplier quote, and delivery plan – and lighter on long-term financial reporting.

For a fuller comparison of the two, the PO funding vs bank loan South Africa guide walks through the difference in detail. Once the requirements are clear, the how to apply for PO funding walkthrough explains the application process step by step. And if you are still comparing providers, the purchase order finance company South Africa guide covers what to look for in a funder.

The Bottom Line on PO Funding Requirements

Purchase order funding requirements South Africa are practical, not bureaucratic. Bring a confirmed deal in the right size range. Bring a clean compliance pack with current SARS, CIPC, and ID. Bring recent business bank statements and a supplier quote. Be honest about anything unusual in your history. Do that, and the assessment moves quickly.

South Africa's SMME funding gap is well documented. The IFC's recent SA SMME finance partnership work shows that even traditional lenders are moving to widen access. Knowing the requirements – and arriving prepared – is how SMMEs actually convert that opportunity into funded contracts.

To start an application once your documents are ready, the Sourcefin funding application form takes about 10 minutes. The Sourcefin purchase order funding service page sets out the full process from there.

Sources & References

Frequently asked questions

What is the minimum requirement to qualify for purchase order funding in South Africa?

The two essentials are a confirmed purchase order, invoice, or award letter from a credible buyer, and your CIPC company registration certificate. Sending your SARS tax PIN, latest 3 months of business bank statements, ID copies, and supplier quote upfront moves the deal review faster. Deals over R1 million also need management accounts, AFS no older than 18 months, and tax return summaries for the past 2 years. Sourcefin's sweet spot starts at R250,000.

Do I need audited annual financial statements to qualify?

It depends on deal size. For deals below R1 million, AFS are not required – recent business bank statements cover what the funder needs to see. For deals over R1 million, you do need Annual Financial Statements no older than 18 months, plus management accounts for the past 3 months and tax return summaries for the past 2 financial years. The deal itself still does most of the talking, but the larger financial pack supports bigger advances.

What credit profile do I need for purchase order funding?

There is no minimum credit score requirement. The funder reviews the credit bureau report as part of the picture, but a low score does not auto-disqualify you. The deal, the buyer, and your delivery plan carry more weight than the bureau number. Disclosure with context about any credit issues is much stronger than silence followed by discovery.

Can I apply if my SARS tax compliance status has lapsed?

Yes, you can still apply. The SARS tax PIN sits in the bonus document group, not the essentials – an application with the purchase order and CIPC certificate can still get moving. A current PIN does speed things up though, so refresh it in parallel via SARS eFiling once any outstanding returns or payments are addressed. If your PIN is current when you apply, send it with the initial submission.

What does the supplier need to provide for the application?

A supplier quote or proforma invoice covering the goods or services you need to deliver against the PO. The quote should be specific enough that the funder can see what is being purchased, the price, and the delivery terms. If you do not have a supplier yet, Sourcefin can sometimes assist with sourcing through its in-house supply chain function and pre-vetted supplier network.

Does the buyer's profile affect whether I qualify?

Yes, often more than your own profile does. A confirmed contract with a major government department, an SOE, or a large corporate is a much easier deal to fund than the same-sized contract with a small private business that has no payment history. The funder needs to be confident that the eventual buyer payment will materialise. That confidence comes from the buyer's track record.

What happens if I do not meet all the requirements yet?

Often the application can still proceed, with the missing piece flagged for completion in parallel. For example, a tax compliance refresh or a CIPC annual return submission can run alongside the deal review. What stops an application entirely is the absence of a confirmed contract or a buyer the funder cannot verify. Documentary gaps are usually solvable. Deal-fundamental gaps are not.

Sourcefin is a South African alternative finance provider that offers purchase order funding and invoice discounting to SMMEs, enabling businesses to fulfil confirmed purchase orders or tenders and unlock cash flow without collateral. Unlike traditional lenders or banks, Sourcefin also provides end-to-end support including supplier sourcing, logistics, project management, and risk oversight.